{kind=link}

What if quick cash costs you more than the problem it solves?

Short-term working capital loans can land in your account the next day and cover payroll, inventory, or emergency repairs when timing is tight.

But they come with short payback windows, frequent withdrawals (daily or weekly), and higher all-in costs than longer loans.

Bottom line: these loans make sense for a one-time cash gap tied to a clear revenue event, but they can squeeze your day-to-day cash or trap you in repeated borrowing if used regularly.

Overview of Short‑Term Working Capital Loan Pros and Cons for Small Businesses

Short-term working capital loans give small businesses fast cash for day-to-day costs. Payroll, inventory, rent, materials, equipment fixes, or short-term growth. They usually come with terms of 24 months or less. Online lenders can approve in minutes and deposit funds as soon as the next business day. That speed and flexible use make them popular when cash is tight. But they also carry higher costs and tighter repayment schedules than traditional loans.

Quick snapshot of pros and cons:

- Pro: Funding can land the next business day after approval

- Pro: Often unsecured, so no collateral or appraisal delays

- Pro: Can be used for almost any short-term business expense

- Con: Repayment terms of 24 months or less create tight payment windows

- Con: Daily or weekly payments pull cash out of operations constantly

- Con: Higher interest rates and fees than long-term loans or bank credit

Advantages of Short‑Term Working Capital Loans for Small Businesses

The biggest advantage? Speed. When payroll hits Friday and a customer payment hasn’t cleared, waiting two weeks for a traditional bank loan isn’t an option. Online lenders approve applications in minutes and can wire funds the next business day. That timeline works when the problem is urgent and short-lived.

Many working capital loans are also unsecured. You don’t put up your truck, equipment, or property as collateral. No appraisal, no lien search, no waiting. If your revenue is steady and your bank statements look clean, you can qualify without risking an asset. That makes the process faster and removes the fear of losing something critical if cash gets tight later.

Key benefits:

- Fast approval and funding: Approvals often happen in minutes. Funds can land the next business day.

- Flexible use: Cover payroll, buy inventory, pay rent or vendor bills, handle emergency repairs, or act on time-sensitive opportunities.

- Unsecured options: Many loans require no collateral, skipping appraisal delays and asset risk.

- Relaxed eligibility: Startups and borrowers with poor credit can often still qualify.

- Real-world fit: If a client owes you $75,000 but won’t pay for 45 days, a short-term loan bridges payroll, rent, and subscriptions until that check clears.

Say a restaurant’s walk-in freezer fails on a Thursday. Replacement parts and labor cost $18,000, and waiting until the next financing cycle means throwing away inventory and closing for a week. A one-day approval and next-day funding window keeps the doors open.

Drawbacks and Risks of Short‑Term Working Capital Loans

The first catch is the repayment window. Most terms run 24 months or less, and borrowers with weaker credit sometimes see even shorter timelines. That compressed schedule means higher monthly (or weekly, or daily) payments compared to a three-year or five-year loan. If revenue dips or timing gets lumpy, those payments squeeze operating cash fast.

Payment frequency is the second pressure point. Instead of one monthly payment, many lenders pull funds daily or weekly through automatic ACH. For a business with daily credit-card sales, that cadence can work fine. But if your invoices go out monthly and clients pay on net-30 terms, daily withdrawals create a mismatch. You’re paying the lender before your own revenue hits the account.

Cost is the third issue. Rates and fees run higher than traditional bank loans. Some lenders quote factor rates instead of APR, which hides the true annualized cost. A factor rate of 1.3 on a six-month advance can translate to an effective APR well above 50 percent. And many lenders charge origination fees up front, say, 4 percent on a $50,000 loan. You receive $48,000, but you still owe the full $50,000 plus interest.

Core risks to watch:

- Compressed timelines: 24 months or less, sometimes much shorter for poor-credit borrowers.

- Frequent withdrawals: Daily or weekly payments strain cash flow if revenue timing is lumpy.

- Higher effective cost: Factor rates and fees can push true APR far above advertised numbers.

- Personal guarantees: Many lenders require unlimited personal guarantees, putting your own assets at risk in default.

There’s also a cycle risk. If you use short-term funding to cover recurring operating shortfalls instead of one-off gaps, you end up borrowing again as soon as you pay off the first loan. Each new advance costs more in fees and interest, and the debt load grows instead of shrinking.

Cost Structure of Short‑Term Working Capital Loans and How to Compare Offers

Understanding what you’re actually paying starts with separating interest from fees and converting any non-APR pricing into an annualized number you can compare. Some lenders advertise low monthly payments but hide high factor rates. Others list an APR that looks reasonable until you add origination fees, underwriting charges, or prepayment penalties.

U.S. business credit cards average close to 24 percent APR. Traditional fixed-rate term loans for qualified borrowers start around 7.2 percent, and variable-rate versions around 7.8 percent. Short-term working capital loans often sit somewhere in between, but they can climb much higher if your credit is weak or the lender uses a factor-rate structure. Always ask for the total repayment amount and the payment schedule, then work backward to the effective cost.

| Pricing Element | What It Means | What to Ask the Lender |

|---|---|---|

| APR (Annual Percentage Rate) | Yearly cost of borrowing, including interest | “What is the APR, and does it include all fees?” |

| Factor Rate | A flat multiplier (e.g., 1.3) applied to the principal; not an interest rate | “Convert this factor rate to an equivalent APR so I can compare it to other offers.” |

| Origination Fee | Up-front charge deducted from your proceeds | “How much do I actually receive after fees, and do I still repay the full amount?” |

| Payment Frequency | How often funds are withdrawn (daily, weekly, bimonthly, monthly) | “What is the exact payment cadence, and can I see a sample payment schedule?” |

| Total Repayment | Principal plus all interest and fees over the full term | “What is the total dollar amount I will repay from start to finish?” |

Here’s a quick example. You borrow $50,000 with a factor rate of 1.25 and a six-month term. Total repayment is $50,000 × 1.25 = $62,500. You pay $12,500 in cost over six months, which works out to an effective APR over 50 percent. If the lender also charges a 4 percent origination fee, you only receive $48,000 but still owe $62,500. That’s the reality behind the advertised number.

Before you sign, get the APR or convert the factor rate yourself, confirm what you’ll actually receive after fees, and map the payment schedule against your cash flow. If the lender won’t give you a clear APR, walk.

Eligibility Requirements and Documentation for Short‑Term Working Capital Loans

Eligibility for short-term working capital loans is often more relaxed than traditional bank underwriting. Lenders look at revenue, time in business, and credit, but many will still approve startups or borrowers with poor personal credit if monthly bank deposits are steady. That makes these loans accessible when a conventional term loan or SBA product won’t work.

Some loans require collateral (your vehicle, equipment, or real estate) but many are unsecured. Unsecured loans move faster because there’s no appraisal or lien filing. The trade-off is higher cost and sometimes a personal guarantee. That guarantee can be limited (capped at a dollar amount) or unlimited (you’re on the hook for the full balance). Always ask which type the lender requires and what happens in default.

Common documentation checklist:

- Business bank statements (last 3–6 months)

- Government-issued ID (driver’s license or passport)

- Proof of revenue (sales records, merchant processor statements, or tax returns)

- Business license or formation documents (LLC, corporation, sole proprietorship)

- Personal and business credit authorization

- Personal guarantee form (if required)

Business credit cards typically need good-to-excellent personal or business credit, so they’re less forgiving than revenue-based working capital products. If your score is below 650, expect stricter terms or outright denial from card issuers, but you may still qualify for a short-term loan based on monthly deposits.

Practical Use Cases for Short‑Term Working Capital Loans

Short-term working capital loans work best when the need is urgent, short-lived, and tied to a clear revenue event or cost savings. They’re not designed for multi-year expansion or buying real estate. But they’re ideal for bridging a temporary gap or capturing a time-sensitive opportunity.

One common scenario is invoice timing. You finish a $75,000 project, but the client won’t pay for 45 days. Payroll, rent, software subscriptions, and vendor bills don’t wait. A short-term loan covers those costs until the invoice clears, then you pay off the loan and move on.

Seasonal businesses face similar pressure. A retailer whose holiday season drives 40 percent of annual revenue needs to buy and stock inventory in October to meet December demand. Suppliers want payment up front. A working capital loan funds the purchase, and holiday sales generate the cash to repay it by January.

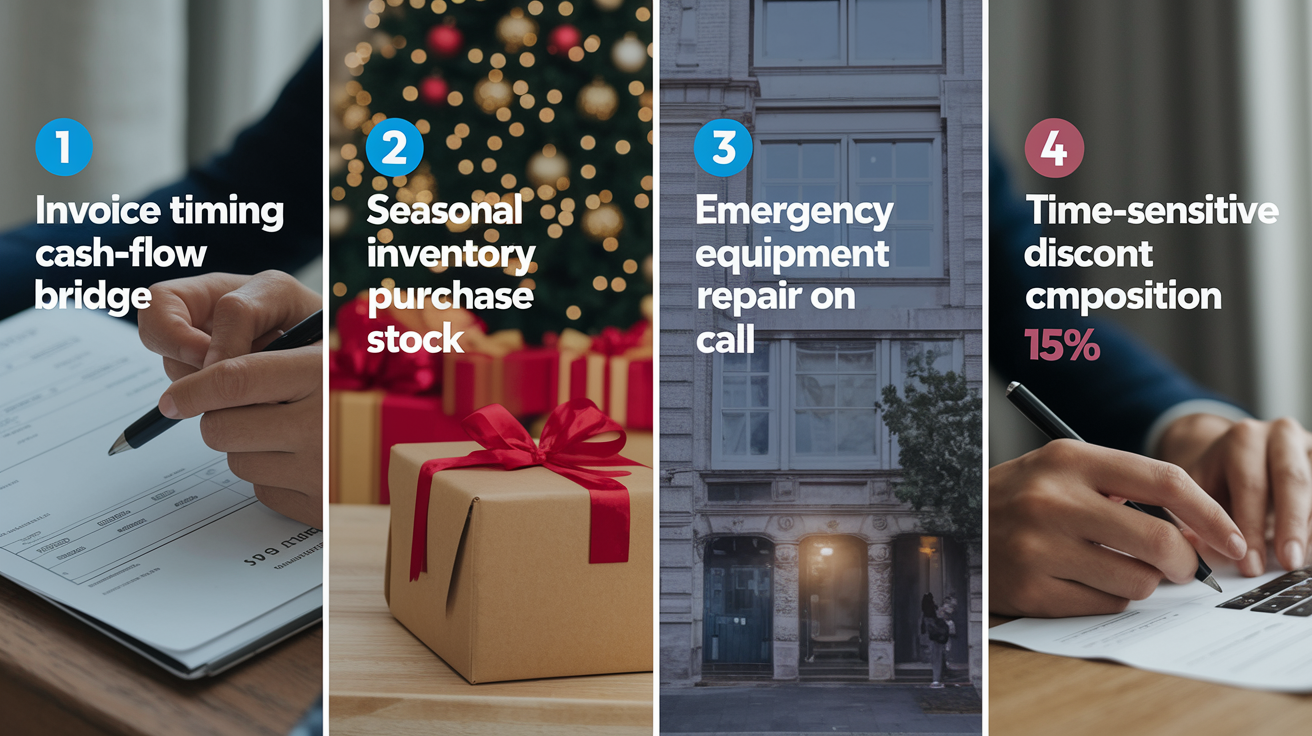

Four real-world use cases:

- Cash-flow bridge: Cover payroll and operating expenses while waiting on a large client payment due in 45 days.

- Seasonal inventory purchase: Buy stock ahead of peak season (holiday, back-to-school, summer) when revenue is still low.

- Emergency equipment repair: Replace a critical asset (freezer, HVAC, delivery truck) to avoid shutdown and lost revenue.

- Time-sensitive discount opportunity: Supplier offers 15 percent off if you pay within 10 days. Short-term funding captures the savings if the loan cost is less than 15 percent.

A restaurant’s walk-in freezer breaks down, and replacement parts plus labor cost $18,000. Waiting for a traditional loan means days of closure and thousands in spoiled inventory. A next-day working capital loan keeps the business open and revenue flowing.

The key in every case is that the loan solves a specific, short-term problem and the business has a clear path to repayment within the term. If the expense is recurring or the revenue source is uncertain, the loan becomes a Band-Aid instead of a bridge.

When Short‑Term Working Capital Loans Make Sense and When to Avoid Them

Short-term working capital loans make sense when you have a profitable business with a temporary cash timing problem. The revenue is coming, but it’s not here yet. Or you need to spend money now to capture a return that exceeds the cost of borrowing. In those cases, speed and flexibility outweigh the higher price.

They don’t make sense for long-term capital expenditures, structural business changes, or funding ongoing operating losses. If you need money for a multi-year expansion, buying property, or covering payroll every month because revenue doesn’t cover expenses, a short-term loan is the wrong tool. The compressed repayment window will make the problem worse, not better.

Decision Checklist

Before you apply, model your cash flow against the proposed payment schedule. If the lender pulls funds daily or weekly, map those withdrawals against your typical deposit timing. If you invoice on net-30 and the lender wants daily ACH, you’ll be paying them before your customers pay you. That mismatch creates stress fast.

Ask the lender for the total repayment amount, not just the monthly payment. Divide total repayment by the amount you’ll actually receive (after fees) to see the true cost. Then compare that number to at least two other options. A business line of credit, a traditional term loan, or even a business credit card if the balance will be paid off quickly.

Five risk indicators that signal you should avoid short-term working capital loans:

- You need funding for a long-term project (property purchase, major expansion, multi-year capex).

- Your revenue is inconsistent or unpredictable, making frequent payments risky.

- The total cost (APR or factor rate plus fees) exceeds the financial benefit or ROI from using the funds.

- You’ve already used short-term credit multiple times in the past year to cover recurring expenses.

- The lender won’t provide a clear APR, total repayment amount, or transparent fee breakdown.

If any of those apply, pause. Either the loan structure doesn’t fit the problem, or the problem isn’t a financing gap. It’s a business model or cash management issue that borrowing won’t fix.

Alternatives to Short‑Term Working Capital Loans for Small Businesses

Short-term working capital loans are one option among many. Depending on your credit, time horizon, and how you plan to use the funds, a different product might cost less, offer more flexibility, or better match your repayment capacity.

Traditional bank term loans offer longer repayment periods (three to five years) and lower interest rates, often starting around 7.2 percent for qualified borrowers. The trade-off is stricter underwriting, longer approval timelines (weeks instead of days), and usually a collateral requirement. If you can wait and you have strong credit, a bank loan costs less over time.

Business lines of credit work like a credit card. You draw what you need up to a limit, pay interest only on what you use, and repay on a flexible schedule. They’re ideal for recurring short-term needs (inventory restocking, seasonal gaps) because you don’t have to reapply every time. Approval is slower than a working capital loan but faster than a term loan, and rates typically sit between short-term loans and traditional bank products.

| Alternative | Best Use Case | Cost Level | Speed |

|---|---|---|---|

| Traditional Bank Term Loan | Long-term capex, expansion, or refinancing existing debt | Low (7–10% APR) | Slow (weeks) |

| Business Line of Credit | Recurring short-term needs, seasonal inventory, flexible access | Medium (10–20% APR) | Moderate (days to week) |

| Business Credit Card | Small purchases paid off monthly; building business credit | High (~24% APR if carried) | Fast (instant if approved) |

| Invoice Financing / Factoring | Selling outstanding invoices for immediate cash | Medium to High (fees vary) | Fast (1–2 days) |

| Merchant Cash Advance (MCA) | Daily credit-card sales; very fast funding | Very High (often 40–100%+ APR equivalent) | Very Fast (same day to next day) |

| SBA Loans / HELOCs | Large amounts, long terms, lowest rates | Very Low (5–8% APR) | Very Slow (weeks to months) |

Business credit cards are useful if you’ll pay the balance in full every month. They build business credit and offer rewards. But if you carry a balance, the average APR near 24 percent makes them expensive. Cards work best for small, predictable expenses you can repay quickly.

Invoice financing (also called factoring) lets you sell outstanding invoices to a lender for immediate cash. The lender advances 70 to 90 percent of the invoice value, collects payment from your customer, then pays you the rest minus a fee. It’s fast and ties repayment directly to receivables, but customers may interact with the third party, which can feel awkward.

Merchant cash advances give you a lump sum in exchange for a percentage of future credit-card sales. Repayment happens automatically as sales come in, so there’s no fixed monthly payment. The cost is very high (often equivalent to 40 to 100 percent APR or more) and daily withdrawals can squeeze cash flow hard. Use them only when no other option fits and the return is certain.

Key Loan Terms and Definitions for Comparing Short‑Term Working Capital Funding

Understanding the language lenders use helps you compare offers accurately and avoid surprises. Here are the core terms you’ll see in short-term working capital agreements.

- APR (Annual Percentage Rate): The yearly cost of borrowing, including interest. Use this to compare loans with similar terms. Lower APR means lower cost.

- Factor Rate: A flat multiplier (like 1.2 or 1.4) applied to the loan amount to calculate total repayment. Not an interest rate. Convert it to APR to see the real cost.

- Origination Fee: An up-front charge, usually a percentage of the loan amount, deducted from the funds you receive. You still repay the full loan amount plus interest.

- Payment Frequency: How often the lender withdraws funds. Daily, weekly, bimonthly, or monthly. More frequent payments reduce available operating cash.

- Personal Guarantee: A legal promise that you’ll repay the loan personally if the business can’t. Can be limited (capped amount) or unlimited (full liability).

- Collateral: An asset (vehicle, equipment, real estate) pledged to secure the loan. The lender can seize it if you default. Unsecured loans require no collateral.

- Prepayment Penalty: A fee charged if you pay off the loan early. Not all lenders charge this, but always ask before signing.

- Total Repayment Amount: The sum of principal, interest, and all fees you’ll pay over the life of the loan. This is the clearest way to compare true cost across offers.

Final Words

When payroll’s due or a supplier needs payment tomorrow, short-term working capital loans can get funds fast, often by the next business day.

This post covered the upside: speed, flexible use, easier approval, and the downsides: higher cost, tighter repayment schedules, and possible personal guarantees.

Weigh the pros and cons of short term working capital loans for small businesses, run the numbers, and pick the option that keeps cash coming in and going out steady. There’s a workable path forward.

FAQ

Q: Are working capital loans a good idea?

A: Working capital loans are a good idea when you need fast, short-term cash for a specific business need and can handle quicker, often costlier repayments without stretching regular cash coming in and going out.

Q: What credit score is needed for a $30,000 loan?

A: The credit score needed for a $30,000 loan depends on the lender; traditional banks often prefer 670–700+, while many online or alternative lenders accept 550–640 if revenue and time in business look solid.

Q: What are the risks of working capital loans?

A: The risks of working capital loans include higher overall cost, frequent daily or weekly payments that can squeeze cash, required personal guarantees, origination fees, and the danger of a repeating debt cycle for recurring expenses.

Q: Who provides the best working capital loans for small businesses?

A: The best providers for working capital loans depend on your priorities: banks for lower rates if you qualify, online lenders for speed and looser credit rules, and alternative lenders for faster, higher-cost funding.