{kind=link}

What if your next payroll depended on an invoice that won’t be paid for 90 days?

Invoice factoring can turn that unpaid invoice into cash this week, but it costs and has rules you need to know.

We’ll cover how much you get up front, what’s held in reserve, the fee structure, recourse versus non-recourse, retainage and lien issues, and the contract language that can stop you from factoring.

Decide fast.

What Subcontractors Need to Know About Invoice Factoring (Direct Answer Section)

Invoice factoring turns unpaid invoices into cash right now. You sell your receivables to a factoring company, get money immediately (usually around 75% of what you’re owed), and the factor collects from the general contractor. When the GC pays, you get the rest minus fees. So if you’ve got a $100,000 invoice sitting there, you’d pocket roughly $75,000 upfront. The other $25,000 sits in reserve until the factor collects, then comes to you after they take their cut.

Subcontractors factor invoices because waiting 60, 90, or 120 days for payment creates real problems. You’ve got payroll every week. Materials don’t buy themselves. Equipment breaks down. Overhead doesn’t pause just because some GC is slow paying. Factoring closes that gap by turning approved work into cash the same week, so you can keep crews paid, stock materials for the next job, or actually bid on bigger projects instead of sitting around waiting for checks.

Construction factoring works a bit differently than regular invoice factoring. Factors verify the GC actually approved your work before they hand over any money. They’ll review lien waivers and pay app docs. Sometimes they check the project owner’s payment track record. And some GC contracts straight up prohibit invoice assignment, so you better check your subcontract language before selling anything.

Five reasons subcontractors use factoring:

- Cash today for payroll, materials, and equipment instead of waiting 30, 60, or 90 days for the GC to get around to paying you.

- Funding that scales with your receivables. Bigger jobs mean more cash without hitting some arbitrary loan limit.

- No debt on the books, and usually no personal guarantee on future revenue. Keeps things cleaner than a traditional loan.

- Someone else chases payments. The factor handles GC follow-up while you focus on actual work.

- Take on more jobs faster. You can bid larger or say yes to additional projects without waiting for old job payments to clear.

Key Costs, Rates, and Fees in Construction Factoring

Factoring fees typically run 1 to 4% of invoice value for each week or month the invoice sits unpaid. These fees get deducted from your reserve when the GC finally pays. Quick-paying GC? Lower fee. Payment drags to 90 or 120 days? Fees stack up and your net proceeds shrink.

Spot factoring (selling one invoice at a time) costs more than contract factoring, where you sell most or all invoices under an ongoing deal. Contract pricing rewards volume with lower rates, but you’re tied to the factor for a set period. Some also tack on setup fees, wire fees, ACH fees, monthly service charges, or minimums. All of it cuts into your net cash.

The biggest risk is not accounting for factoring fees in your bids. If you price jobs assuming 100% invoice value and only receive 96 or 97% after fees, your profit just disappeared. Run the numbers before you bid. Include estimated factoring cost and reserve timing in your break-even, or the “discount” comes straight from your margin.

| Cost Type | Description | Impact on Subcontractors |

|---|---|---|

| Invoice fee (1–4%) | Charged per week or month the invoice is outstanding | Cuts net proceeds directly; accumulates if GC pays slowly |

| Setup and service fees | One-time or monthly charges for account admin | Fixed cost regardless of invoice volume |

| Wire and ACH fees | Per-transaction charges for funding | Small individually, adds up over many invoices |

| Minimum volume requirements | Some factors require minimum monthly receivables | Forces you to factor invoices you’d rather carry yourself |

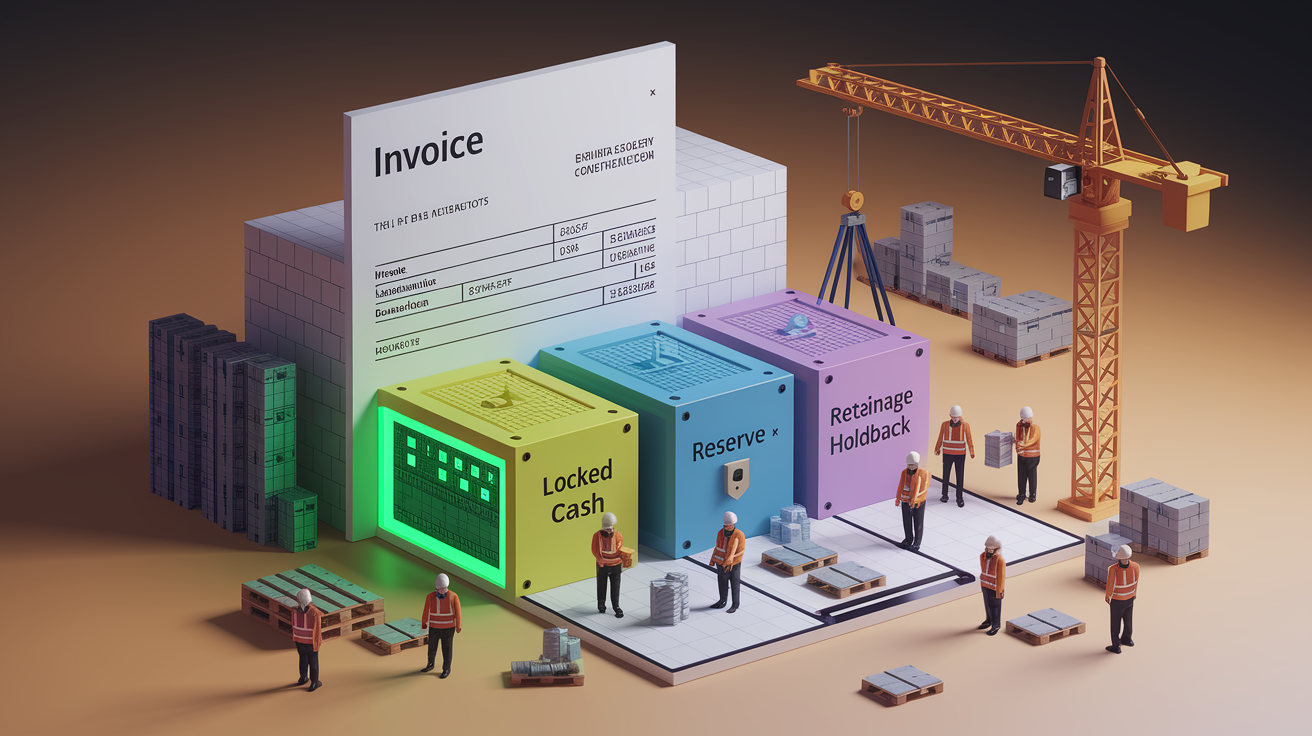

Understanding Advance Rates, Reserves, and Holdbacks

Advance rates for subcontractors usually sit around 70 to 80%, with 75% being pretty standard. The factor holds the remaining 20 to 30% in reserve until the GC pays in full. Your reserve gets released when the factor collects, minus their fee.

Construction jobs complicate this in ways that can reduce advance rates:

- Retainage provisions in your subcontract (often 5 to 10% held by the GC until project wraps) lower the collectible amount, so the factor might reduce the advance.

- Unapproved pay applications or disputed line items delay funding, since factors verify work approval before releasing anything.

- Lien exposure from unpaid material suppliers or lower-tier subs can cause factors to hold extra reserve or demand lien releases before funding.

- Progress billing on long projects can create partial advances, with full reserve release only after final payment and closeout.

In practice, if you’ve got a $100,000 invoice with 10% retainage, the collectible amount is $90,000. A 75% advance on $90,000 is $67,500 upfront, with roughly $22,500 held in reserve. When the GC pays and retainage eventually gets released, you receive the balance minus fees. If you expected $75,000 upfront, that difference can squeeze cash flow mid-project.

Recourse vs Non-Recourse Factoring for Subcontractors

Recourse factoring means you’re on the hook if the general contractor doesn’t pay. The factor advances cash, but if the GC goes bankrupt, disputes the invoice, or simply ghosts you, you have to repay the advance. Non-recourse factoring shifts that credit risk to the factor, so if the GC fails to pay because of insolvency, the factor eats the loss and you keep the advance.

Non-recourse sounds safer. But it comes with limits. Most non-recourse agreements only cover customer bankruptcy, not payment disputes, slow pay, or work quality issues. If the GC refuses payment because of some disagreement over scope or completion, you’re still responsible for repaying the advance. Non-recourse also costs more, since the factor assumes collection risk and prices that into fees.

Things to consider when choosing recourse vs non-recourse:

- Check your GC’s payment history before opting for recourse. If they’re financially stable and pay consistently, recourse pricing might save you money without adding real risk.

- Understand non-recourse exclusions. Read the contract to see what actually triggers coverage and what doesn’t. Dispute-related non-payment rarely qualifies.

- Weigh cost vs risk. If non-recourse adds 0.5 to 1% per invoice and your GCs almost never default, recourse is probably the better deal.

How Construction-Specific Factoring Works (Verification, Lien Rights, and Project Controls)

Construction factoring requires verification of approved work before funding. Factors don’t just buy an invoice based on your word. They confirm the general contractor signed off on the pay application, the work matches approved scope, and there aren’t any open disputes or liens that could block payment. This protects both you and the factor from funding invoices that won’t actually get paid.

Lien laws add another layer. In many states, mechanics’ lien statutes require material suppliers and lower-tier subcontractors to be paid before a prime sub can take proceeds from factored invoices. Some factors use “funds control” processes, directly paying your suppliers from the advance to prevent lien filings and ensure clean payment sequencing. If you don’t manage lien releases properly, the factor may hold back portions of the advance until all downstream parties sign waivers.

Notice of Assignment is standard in construction factoring. The factor sends formal notification to the GC, instructing them to pay the factor directly instead of you. Some GC contracts prohibit or restrict assignment of receivables without written consent, so you need to review your subcontract language and get approval before factoring. Skip this step and you could be in breach of contract with legal exposure.

Core construction-specific steps in the factoring process:

- Approved pay application or invoice submitted to the factor with GC sign-off or approval documentation.

- Verification of scope and work completion, often cross-checked against contract schedules and prior payment history.

- Lien waiver collection from suppliers and lower-tier subs, either before funding or paid directly from the advance by the factor.

- Notice of Assignment sent to the GC, redirecting payment to the factor and confirming invoice validity.

Funds control keeps the process clean. Instead of you receiving the advance and then scrambling to pay suppliers, the factor disburses payments in the correct order, reducing lien risk and simplifying closeout. This extra operational work is why construction factoring often costs slightly more than general commercial factoring.

Eligibility Requirements and Required Documentation

Most construction factors want to see approved invoices, bank statements, and identification before they fund. Approved invoices mean the GC signed the pay application or provided written confirmation that the work is complete and payment is authorized. Factors also review your payment history with that GC and check the project owner’s creditworthiness, since they’re underwriting the entire payment chain.

Lien waivers are often required before funding or included in the advance distribution. If you haven’t paid your material supplier yet, the factor may pay them directly from your advance and require a signed waiver in return. This protects the factor from future lien claims that could tie up the invoice proceeds.

| Document | Purpose | Notes |

|---|---|---|

| Approved pay application or invoice | Proves work is complete and approved by GC | Must include GC signature or written approval |

| Subcontract or purchase order | Confirms scope, payment terms, and assignment rights | Factor reviews for anti-assignment clauses |

| Lien waivers (conditional or unconditional) | Clears downstream payment obligations and lien exposure | Often required before advance or paid from advance |

| Bank statements (last 3 months) | Shows cash flow, deposit history, and financial health | Helps factor assess overall business stability |

| Business and personal ID | Verifies identity and business registration | Standard underwriting and compliance requirement |

Digital submissions speed up the review. Uploading clean PDFs of signed pay apps, waivers, and statements through a secure portal cuts turnaround time from days to hours. Factors with construction experience often provide templates and checklists to help you organize documentation correctly the first time.

Impact on General Contractor and Client Relationships

Factoring usually requires notifying the general contractor that invoices have been assigned to a third party. The Notice of Assignment tells the GC to pay the factor directly instead of you. Some GCs are used to this and have standard procedures for processing factored invoices. Others might view it as a red flag about your cash position or add administrative friction to their payables process.

Disputes and collections can strain relationships if not handled professionally. A good factor understands construction payment cycles and communicates respectfully with GCs. A bad factor may send aggressive collection letters, call repeatedly, or turn minor issues into major conflicts in ways that damage your reputation. Before signing with a factor, ask how they handle collections, what their communication approach looks like, and whether you have approval rights over any steps they take.

Three ways to protect GC relationships when factoring:

- Communicate early. Let your GC know you’re using factoring and explain the Notice of Assignment process before they receive paperwork from a third party.

- Set clear expectations with the factor. Require written approval for any collection communication beyond standard payment reminders, and confirm they won’t threaten liens or legal action without your consent.

- Keep dispute resolution in-house. If a payment issue arises, work directly with the GC to resolve it before the factor gets involved. Most factors will pause collections if you’re actively addressing a legitimate dispute.

Many subcontractors use factoring selectively, only on invoices from GCs with slower payment cycles, while continuing to collect directly from GCs who pay quickly. This keeps factoring costs low and limits third-party involvement to situations where the cash-flow benefit justifies the relationship complexity.

Choosing the Right Factoring Company for Subcontractors

Not all factors understand construction. General commercial factors may not verify approved work, underwrite the project chain, or know how to handle lien waivers and retainage. You need a factor with real construction experience, ideally one that works primarily with subcontractors and understands mechanics’ lien law, pay application workflows, and GC payment behavior.

Seven questions you should ask before signing:

- What’s your advance rate, and how do retainage and progress billing affect it? Get specific numbers based on typical construction invoices.

- What are your fees, and how are they calculated? Demand a written fee schedule showing weekly or monthly rates, setup costs, wire fees, and any minimums.

- Do you verify work approval and underwrite the GC and project owner? Construction factors should confirm payment chain strength, not just your credit.

- How do you handle lien waivers and downstream supplier payments? Ask if they use funds control and pay suppliers directly from advances.

- What are your recourse terms? Clarify whether you’re responsible for non-payment due to GC disputes, insolvency, or both.

- How long is the contract, and what are the termination terms? Avoid auto-renew clauses longer than 12 months and confirm you can exit without penalty if the relationship doesn’t work.

- Can you provide references from other subcontractors in my trade? Ask for contacts who can confirm advance speed, fee transparency, and collections professionalism.

Red flags include unclear or changing fee formulas, aggressive third-party collections without your approval, low advance rates under 70%, reluctance to provide written terms, and lack of familiarity with construction-specific documentation. If a factor treats your invoices the same way they’d factor retail receivables, walk away.

Check contract compatibility with your GCs. If your subcontracts include anti-assignment clauses or require GC consent before factoring, confirm the factor has a process for obtaining waivers or working within those restrictions. Choosing a factor experienced in your region and trade increases the odds they already have relationships or procedures that smooth approval.

Alternatives to Invoice Factoring for Subcontractors

Invoice factoring is one tool among several. Bank lines of credit typically cost less, often 7 to 12% APR compared to effective annualized factoring rates of 12 to 40% or more, depending on invoice aging. The tradeoff is speed and flexibility. Banks require strong credit, financial documentation, and collateral, and approval can take weeks. Factoring can fund in days with lighter underwriting, making it better for urgent needs or newer businesses without deep credit history.

SBA loans and equipment financing offer lower rates and longer terms but tie capital to specific purchases and involve fixed monthly payments. If you need cash for payroll or materials across multiple jobs, these options are less flexible than factoring, which scales with receivables and has no fixed repayment schedule.

Purchase-order financing funds material purchases before you invoice the GC, useful when you need to buy supplies upfront for a large job. Retainage financing specifically advances the 5 to 10% holdback that GCs retain until project completion, solving a different cash-flow gap than invoice factoring. Some subcontractors blend these tools, using PO financing to buy materials, invoice factoring to cover payroll and overhead, and retainage financing to unlock holdbacks at closeout.

Internal accounts receivable management is the cheapest alternative. Speeding collections by sending digital invoices with payment links, following up promptly, offering small early-payment discounts, or negotiating shorter net terms with GCs can reduce the need for factoring entirely. If you can get paid in 30 days instead of 60, you may not need outside capital at all.

Four alternatives and when they make sense:

- Bank line of credit when you have solid credit, time to wait for approval, and predictable borrowing needs across multiple projects.

- Equipment loans or SBA financing when the capital is for a specific asset purchase and you can handle fixed monthly payments.

- Purchase-order or supply-chain financing when your cash squeeze is upfront material costs, not post-invoice waiting periods.

- Retainage financing when the GC is holding 5 to 10% and you need that cash before project closeout, but invoices themselves are being paid on time.

Compare total cost over the life of the invoice or project. A 2% weekly factoring fee on a 60-day invoice works out to roughly 17% effective annualized cost. A bank line at 10% APR is cheaper if you qualify. Run the numbers and weigh cost against speed, approval likelihood, and operational fit.

Common Pitfalls, Risks, and Red Flags in Subcontractor Factoring

Hidden fees are the most common pitfall. Setup charges, monthly service fees, wire fees, ACH fees, and minimum volume requirements can add hundreds or thousands of dollars to your total cost. Always ask for a complete written fee schedule with examples showing total cost on invoices of different sizes and aging periods.

Long auto-renew contract terms lock you in when the relationship isn’t working. Some factors use 12, 24, or even 36-month agreements with automatic renewal unless you provide 60 or 90 days’ notice. If the factor’s service declines, fees increase, or you find a better option, you’re stuck. Look for agreements with clear termination rights and reasonable notice periods.

Five red flags that should stop you from signing:

- Opaque or changing fee formulas that make it impossible to calculate your net proceeds in advance.

- Required assignment of all receivables, forcing you to factor every invoice even when you don’t need cash, or giving the factor control over your operating bank account.

- Aggressive collections practices that contact GCs without your approval, threaten liens prematurely, or damage customer relationships.

- Advance rates below 70% or excessively high reserve holdbacks that don’t match industry norms for construction invoicing.

- Lack of construction expertise, such as inability to explain lien waiver processes, retainage handling, or project-chain underwriting.

Margin risk increases when you don’t build factoring fees into bids. If you assume full invoice value when estimating job cost and profit, the 2 to 4% factoring discount comes straight out of your margin. On a tight bid, that can turn a small profit into a loss. Always include estimated factoring cost in your pricing model before you submit a proposal.

Some factors pressure you to give personal guarantees beyond the invoices being factored, effectively turning factoring into a personal loan. Factoring should be non-recourse or limited-recourse tied to the specific receivable, not a blanket personal liability for business operations. Read guarantee language carefully and push back on overly broad terms.

Real-World Examples: When Factoring Helps Subcontractors

Factoring makes the most sense when waiting for payment creates an immediate operational problem. A concrete subcontractor finishing a $200,000 pour on net 90 terms needs to meet payroll and buy materials for the next job before the GC pays. Factoring that invoice unlocks $140,000 to $160,000 in cash within days, keeping the business moving instead of turning down new work or missing payroll.

Equipment breakdowns create sudden capital needs that factoring can solve. An HVAC subcontractor’s van breaks down mid-project, and repairs or replacement cost $15,000. Instead of waiting 60 days for a $50,000 invoice to clear, factoring advances $37,500 immediately, covering the equipment cost and keeping the crew on schedule. The fee is a few hundred dollars, but the alternative is lost revenue from delayed work or unhappy customers.

Growth opportunities often require faster cash cycles. A framing subcontractor is invited to bid on a $2,000,000 project, but doesn’t have the working capital to buy lumber and pay crews upfront while waiting months for GC payments. Factoring converts each progress invoice into immediate cash, letting the subcontractor execute the large job without turning it down or bringing in equity investors.

Three situation types where factoring is commonly used:

- Payroll and crew management when invoice aging creates gaps between paying workers and receiving GC payments, especially on jobs with net 60, 90, or 120 terms.

- Materials and supply purchases for upcoming jobs when cash is tied up in unpaid invoices from prior work, and suppliers require payment upfront or on short net terms.

- Bidding and growth capacity to take on larger projects or multiple simultaneous jobs that exceed available working capital without outside funding.

Factoring is less useful when GCs pay quickly and reliably. If you’re consistently receiving payment within 30 days and have enough cash reserves to cover the gap, the cost of factoring outweighs the benefit. It’s a tool for solving specific cash-flow problems, not a permanent financing strategy for businesses with healthy payment cycles.

Key Things Subcontractors Should Keep in Mind

Include factoring fees in your bids before you submit pricing. If you plan to factor invoices to cover cash flow, build that 2 to 4% cost into your job estimate so it doesn’t erase profit. Run the math on typical invoice aging for each GC and calculate the effective cost of factoring before you commit to pricing that assumes full invoice value.

Confirm your subcontract allows invoice assignment before signing with a factor. Many GC agreements include anti-assignment clauses or require written consent before you can sell receivables. Factoring an invoice that’s contractually non-assignable can put you in breach and create legal exposure or payment refusal by the GC.

Review lien implications with an attorney, especially if you rely on material suppliers or lower-tier subcontractors. Mechanics’ lien laws in your state may require you to pay suppliers from factoring advances before taking cash yourself, and failing to manage lien waivers correctly can delay funding or create liability.

Compare factoring cost to alternatives and only use it when the benefit justifies the expense. If a bank line of credit, short-term loan, or internal cash management can solve the same problem at lower cost, factoring may not be the right fit. Factoring works when speed, flexibility, and the ability to scale matter more than minimizing financing cost.

Four major considerations before factoring:

- Build fees into bids to protect job-level profitability and avoid margin erosion from factoring discounts.

- Confirm contract permissibility by reviewing subcontract assignment clauses and obtaining GC consent if required.

- Understand lien law and supplier payment obligations to avoid funding delays or legal exposure from unpaid downstream parties.

- Compare total cost to bank credit, equipment loans, and internal AR management to ensure factoring is the most practical solution for your situation.

Factoring is a useful working-capital tool when deployed strategically. It converts payment delays into immediate cash, letting subcontractors meet payroll, buy materials, and bid on larger jobs without waiting months for GC checks. The key is doing the math, confirming contract and lien compatibility, choosing an experienced factor, and using it only when the cost-benefit equation makes sense for your business.

Final Words

Invoices are waiting and payroll’s due. This article walked through how invoice factoring works for subcontractors, invoice to advance, factor collects, reserve released. Typical advance is about 75 percent (for example, a $100,000 invoice becomes a $75,000 advance). We also covered fees, recourse vs non-recourse, construction checks, required docs, and the main red flags.

Run the numbers before you sign. Gather approved invoices and GC verifications, compare fees, and pick a factor with construction experience. With the right fit, invoice factoring for subcontractors what to know becomes a practical tool to keep crews paid and jobs moving.

FAQ

Q: Is invoice factoring a good idea? What are the cons of invoice factoring? What is the average cost of invoice factoring?

A: Invoice factoring is a good idea when you need fast cash, but it reduces profit. Fees typically run 1–4% of the invoice per week or month; advances are often ~70–80% with a 20–30% reserve.

Q: How to invoice as a subcontractor?

A: To invoice as a subcontractor, submit a clear pay application listing GC-approved amounts, contract reference, invoice number and retainage. Attach required lien waivers or pay-app docs and follow the GC’s billing schedule.