{kind=link}

Think your business assets will cover an SBA 7(a) loan?

Think again.

The SBA expects lenders to secure loans over $25,000, but the rule isn’t meant to punish.

It’s about what a lender can actually recover in a forced sale.

This post walks you through when collateral is required, which business and personal assets qualify, how lenders apply steep discounts, and when your home might be on the table.

Read on so you can plan what to pledge and avoid surprises at closing.

Complete Overview of SBA 7(a) Loan Collateral Rules and When Collateral Is Required

The SBA requires lenders to take collateral on 7(a) loans above $25,000, but the rules are practical, not punitive. The goal is to make the loan “fully secured” whenever possible by counting available business and personal assets at their discounted liquidation value. Got enough business assets to cover the loan? Personal real estate usually stays out of it. If you don’t, the lender will look at what else is available, including personal property, and decide whether the loan still makes sense based on cash flow and other factors.

Loans of $25,000 or less don’t require collateral under SBA guidelines. For loans between $25,001 and $350,000, lenders must first pledge all financed and business fixed assets, then trade assets like inventory and receivables. Personal real estate only comes into play if business collateral doesn’t fully secure the loan. Above $350,000, lenders typically pursue all available collateral, including personal residential or investment real estate, until they reach full security or document why they can’t.

The SBA applies heavy discounts when valuing collateral. Equipment you bought for $100,000 might count for $50,000 or less. Real estate appraisals get cut by 15% or more to reflect forced sale conditions. And here’s something critical that gets missed: the SBA guarantee itself doesn’t count as collateral. It protects the lender’s exposure, but it doesn’t reduce the amount of collateral the lender is required to pursue. That means even on a loan where the SBA guarantees 75%, you’re still expected to pledge assets as if the loan were 100% at risk.

Key requirements to know before you apply:

- Loans above $25,000 require collateral. Loans of $25,000 or less do not.

- All available business assets must be pledged first, before personal real estate is considered.

- The SBA heavily discounts asset values to reflect liquidation conditions, not market or book value.

- The SBA guarantee isn’t collateral and doesn’t reduce the collateral the lender must take.

- Insufficient collateral doesn’t automatically disqualify you if cash flow is strong and all available assets are pledged.

Asset Types Commonly Used as SBA 7(a) Loan Collateral

Lenders prioritize tangible business assets that can be sold or repossessed quickly. Commercial real estate, equipment, and inventory sit at the top of the list. Accounts receivable and cash deposits count, but at steep discounts. Personal assets, especially personal real estate, are pulled in only after business collateral is exhausted or when the loan is large enough that business assets alone can’t cover it.

Intangible assets like goodwill, franchise rights, and intellectual property are accepted in theory but heavily discounted in practice, sometimes to zero. Life insurance policies are often required to be assigned to the lender, but the policy’s cash value typically isn’t counted toward collateral. And if you try to shield real estate by placing it in a personal trust or LLC, expect the lender to dig into ownership and treat it as available collateral if you control the entity.

Commonly accepted collateral includes:

Commercial real estate. Owner occupied buildings, warehouses, retail space, and land. First choice for large loans.

Business equipment and machinery. Vehicles, manufacturing equipment, tools, computers. Valued conservatively, especially if used.

Inventory and raw materials. Counted at a fraction of book value, typically 10%, because it’s perishable or hard to liquidate.

Accounts receivable. Also discounted heavily, around 10% of book value, because collection is uncertain.

Furniture and fixtures. Desks, shelving, signage. Counted at roughly 10% of net book or appraised value.

Personal real estate. Your home or investment property, required when business assets don’t fully secure the loan and available equity exists.

SBA 7(a) Collateral Valuation, Discounts, and Liquidation Standards

Collateral isn’t valued at what you paid, what it’s insured for, or what you think you could sell it for on a good day. Lenders value collateral at what they expect to recover in a forced sale, after costs, delays, and depreciation. The SBA sets maximum allowable percentages for each asset type, and lenders stick to them. These discounts can be jarring if you’re used to thinking in terms of replacement cost or retail value.

Real estate gets the most favorable treatment, but even then, the SBA caps improved commercial real estate at 85% of appraised market value. Unimproved land drops to 50%. Equipment purchased new for the project might count at 75% of the invoice price, minus any prior liens. Used equipment falls to 50% of net book value unless you provide an orderly liquidation appraisal, which can push it up to 80%. Furniture, fixtures, inventory, and receivables all get discounted to 10% or less because they’re hard to move or collect in a distressed scenario.

| Asset Type | Max SBA Allowable Value % | Notes |

|---|---|---|

| Improved real estate | Up to 85% of market value | Requires third party appraisal |

| Unimproved/vacant land | Up to 50% of market value | Higher discount due to sale difficulty |

| New equipment (excl. furniture) | Up to 75% of purchase price | Less any prior liens |

| Used equipment (excl. furniture) | 50% of net book; up to 80% with orderly liquidation appraisal | Appraisal may be required for high value items |

| Furniture & fixtures | Up to 10% of net book or appraised value | Low recovery expectation |

| Inventory | Up to 10% of current book value | Perishable or industry specific |

| Accounts receivable | Up to 10% of current book value | Collection risk heavily discounted |

Personal Guarantees and the Role of Personal Assets in SBA 7(a) Collateral

Every owner with 20% or more ownership in the business must sign an unlimited personal guarantee. That guarantee gives the lender the right to pursue your personal assets if the business defaults, but it doesn’t replace the requirement to pledge specific collateral. The personal guarantee and collateral requirements work in tandem. One doesn’t eliminate the other.

If business assets don’t fully secure the loan, the lender will look at your personal real estate. That might be your primary residence or investment property you own outright or with equity. The SBA excludes property where available equity is less than 25% of fair market value, so if your home is worth $400,000 and you owe $320,000, the lender typically won’t require a lien. Some states prohibit pledging a primary residence for business debt entirely, and the lender must follow those restrictions.

Spouse owned property is generally excluded unless your spouse is also a required guarantor (because they own 20% or more), or the combined ownership of you, your spouse, and any minor children reaches 20%. Transferring property to a spouse right before applying won’t work. Lenders scrutinize recent ownership changes and will treat the property as available if the timing looks like an attempt to shield assets. The equity in any pledged personal real estate must be documented by independent sources like tax assessments or appraisals, not just what you wrote on your personal financial statement.

Lien Positions, UCC Filings, and Documentation Needed to Secure SBA 7(a) Collateral

Lenders perfect their security interest in collateral by filing UCC-1 financing statements for business personal property and recording mortgages or deeds of trust for real estate. A UCC-1 is a public notice that the lender has a claim on your equipment, inventory, receivables, and other movable business assets. The mortgage filing does the same thing for real property. Both filings establish lien priority. Who gets paid first if assets are sold.

Lenders strongly prefer first lien position on all collateral. If another lender already holds a lien, the SBA lender may still take a junior or subordinate lien, but they’ll discount the collateral value even further to account for the senior lender’s claim. On personal real estate, the lender may record a mortgage for the full loan amount, or they may limit the lien to the collateral shortfall or 150% of available equity to reduce state recording taxes or title insurance costs. Title insurance is usually required on real estate collateral to confirm clear title and protect the lender from prior claims.

Key collateral documentation you’ll encounter:

UCC-1 financing statement. Filed with the state to claim business personal property.

Security agreement. The contract that grants the lender rights to specific collateral.

Mortgage or deed of trust. Recorded document creating a lien on real estate.

Title insurance and lien searches. Required to verify ownership and identify existing encumbrances before closing.

What Happens When There Is Insufficient SBA 7(a) Collateral

A collateral shortfall doesn’t kill the deal. The SBA allows lenders to approve loans even when available collateral doesn’t fully cover the loan amount, as long as the lender has taken all available collateral and documented the shortfall. What matters is that you’ve pledged everything you reasonably can, and the lender believes the loan will be repaid based on cash flow, owner equity, and other compensating factors.

When collateral falls short, lenders look harder at debt service coverage ratio, operating history, owner injection, and liquidity. If your business generates $200,000 in annual cash flow and the loan payment is $60,000, that 3.3x coverage can offset a collateral gap. A larger down payment, say 20% instead of 10%, also reduces the lender’s risk and makes up for limited collateral. Additional personal guarantors or willingness to pledge other personal assets can help, too.

If compensating factors aren’t strong enough, the lender may reduce the loan size to match available collateral, shorten the term to lower total exposure, increase the interest rate, or require additional equity. In some cases, they’ll decline the loan. But the key point is this: collateral shortage alone doesn’t disqualify you if the rest of the deal is solid and you’re transparent about what’s available.

Lenders rely on these compensating factors when collateral is insufficient:

Strong cash flow and debt service coverage ratios. 1.25x or higher preferred.

Higher owner equity injection or down payment. 15% to 25% instead of 10%.

Additional personal collateral or guarantees from other owners or family members.

Clean credit history, long operating history, and documented demand for the business.

SBA 7(a) Collateral Exceptions, Thresholds, and Special Cases

Loans of $25,000 or less are exempt from collateral requirements entirely under SBA policy. Lenders may still ask for collateral on small loans as a matter of practice, but the SBA doesn’t require it. For loans between $25,001 and $350,000, including Community Advantage loans, the rules are more flexible. Lenders must take all available business assets first, but personal real estate is required only if business collateral doesn’t fully secure the loan.

Entity held real estate can be pledged as collateral if the borrower owns a majority interest in the entity, even if the property is titled in an LLC or trust. Collateral release or substitution is allowed during the life of the loan but requires lender approval and SBA authorization. Common scenarios include selling a pledged property and replacing it with a new one, or releasing business equipment after it’s fully depreciated or sold, as long as the loan balance is paid down enough to maintain adequate security.

| Exception Type | Description |

|---|---|

| Loans ≤ $25,000 | No collateral required under SBA policy, though lender may still request it. |

| Loans $25,001–$350,000 | Business assets pledged first; personal real estate required only if business collateral insufficient. |

| Collateral release or swap | Possible with lender and SBA approval, typically when loan balance declines or asset is replaced. |

Numeric Examples Showing How SBA 7(a) Collateral Requirements Work

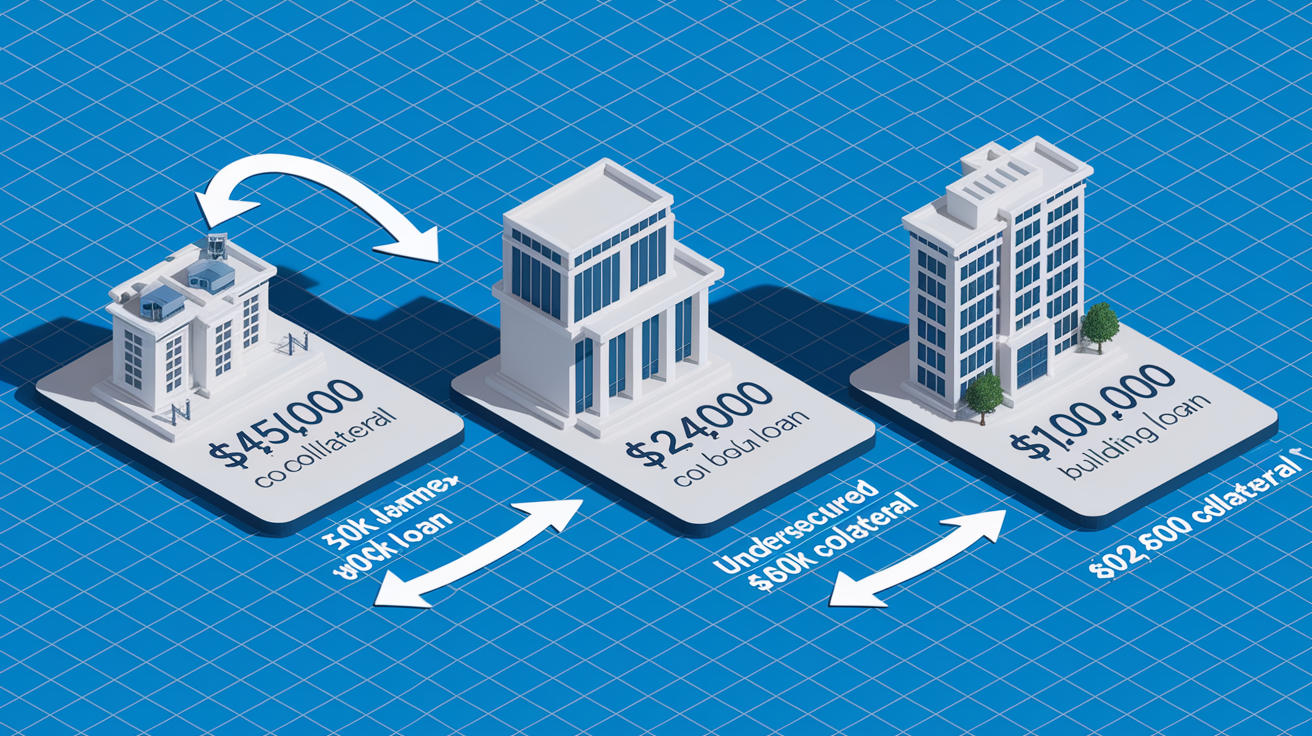

A buyer wants to acquire a business for $500,000 and plans to put down $50,000, requesting an SBA 7(a) loan of $450,000. The business owns equipment and inventory appraised at $300,000. After applying SBA discount rates, 50% on used equipment, 10% on inventory, the realizable collateral value drops to roughly $180,000. The lender documents a collateral shortfall of $270,000. To close the loan, the lender may require the buyer to pledge personal real estate with at least that much available equity, or increase the down payment to $150,000 to reduce the loan to $350,000 and avoid the personal real estate requirement.

A borrower requests $150,000 to expand a service business. Available business collateral includes office furniture valued at $8,000 and used equipment valued at $40,000. After discounts, the lender counts $4,000 for furniture and $20,000 for equipment, totaling $24,000. The loan is undersecured by $126,000. The lender takes a blanket UCC on all business assets, requires personal guarantees from all owners with 20% or greater stakes, and asks the borrower to either inject $50,000 more equity or allow a lien on investment property with $150,000 in available equity.

An owner operator buys a commercial building for $1,000,000 with a $200,000 down payment and a $800,000 SBA 7(a) loan. The building appraises at $1,050,000. At 85% loan to value, the allowable collateral value is $892,500, fully covering the $800,000 loan. The lender records a first mortgage on the property, files a UCC-1 on business assets housed in the building, and requires a personal guarantee from the 100% owner. No additional personal real estate is required because the primary collateral fully secures the loan.

Three lessons from these examples:

Collateral is always discounted, sometimes steeply, so book value or purchase price rarely equals collateral value.

Shortfalls can be closed with higher equity, shorter loan terms, or pledging additional personal assets.

Real estate collateral, especially owner occupied commercial property, provides the cleanest path to full security.

Preparing Your Collateral Package for an SBA 7(a) Loan Application

Start by listing every asset the business owns and every piece of real estate you personally control. Lenders will ask for equipment lists with make, model, year, and estimated value. They’ll want inventory counts and accounts receivable aging reports. If you own commercial real estate or plan to buy it with the loan, get a recent appraisal or broker opinion of value. Personal financial statements must include your home and any investment properties, with current mortgage balances and estimated market values backed by tax assessments or appraisals, not guesses.

Expect the lender to run UCC searches on your business and personal name to identify existing liens. If another lender already has a security interest in your assets, you’ll need to disclose it and provide payoff or subordination terms. Life insurance policies with cash value may be required to be assigned to the lender as additional security, even though they typically won’t count toward collateral value. The stronger and more organized your collateral documentation, the faster underwriting moves and the less likely you’ll face requests for personal real estate liens.

Tasks to complete before submitting your application:

Compile a detailed equipment and fixed asset list with ages, purchase prices, and current estimated values.

Gather real estate documentation: deeds, recent appraisals, mortgage statements, and tax assessments for business and personal property.

Prepare a personal financial statement listing all real estate, vehicles, investments, and significant personal property.

Request an accounts receivable aging report and current inventory valuation from your accountant.

Run your own UCC search to identify existing liens and prepare payoff or subordination letters if needed.

Final Words

You know the core rules now: when collateral is required, the $25,000 and $350,000 thresholds, which business and personal assets lenders prefer, and how the SBA heavily discounts value.

Use that to map what you can pledge and what to expect if coverage falls short—improve cash coming in and going out, add equity, or offer stronger guarantees.

Gather the appraisal-ready docs from the prep section and talk to a lender who understands sba 7a loan collateral requirements; with clear numbers and the right prep, you can get a workable answer and keep your plan moving.

FAQ

Q: Does an SBA 7A loan require collateral?

A: An SBA 7(a) loan requires collateral for loans over $25,000; loans $25,000 or less typically need none. For $25,001–$350,000 lenders pledge all available business assets first; real estate only if needed.

Q: How hard is it to get an SBA 7A loan? What disqualifies you from an SBA loan? What are the common reasons 7A loans are denied?

A: Getting an SBA 7(a) loan can be tough if you have weak cash coming in, poor personal or business credit, under two years in business, incomplete documentation, low owner equity, or an ineligible business.