{kind=link}

Did you know the IRS usually lets you deduct interest on short-term working capital loans, but only if the money was actually spent on the business and the loan looks like real debt?

If you borrow to cover payroll, restock inventory, or bridge a slow season, that deduction can cut your tax bill fast.

This post explains the core rules, what counts as business use, when interest is deductible for cash versus accrual taxpayers, how loan type affects deductibility, and the documentation you must keep to prove it.

Core Rules for Deducting Interest on Short‑Term Working Capital Loans

When you borrow to cover payroll, restock inventory, or keep the lights on, the IRS usually lets you deduct the interest you pay. The core rule? Interest on loans used for legit business purposes is typically deductible, often 100% of what you paid for the year if you meet IRS criteria. The loan needs to be real debt with a real lender, you’ve got to be legally on the hook for repayment, and the money actually has to get spent on business.

Short‑term working capital loans usually run anywhere from 3 months to about a year. If you borrow in April, spend the funds on business expenses in April, and pay the loan back by December, you can usually deduct all the interest paid in that single tax year. That’s one advantage of short‑term financing for tax purposes. The deduction hits fast.

The “spend‑it” rule matters. Interest becomes deductible only after you’ve spent the borrowed funds on business. If the loan proceeds sit idle in your bank account, the IRS treats that as an investment, and you can’t deduct the interest. Once you pay vendors, cover payroll, or buy inventory with that cash, the interest tied to those funds becomes deductible.

Deductible vs. Non‑Deductible Interest Scenarios:

Deductible: Interest on a working capital loan used to pay inventory, payroll, rent, or operating expenses during the tax year.

Deductible: Interest on a line of credit where you’ve drawn funds and spent them on business costs.

Not deductible: Interest on loan funds left sitting unused in a business checking account.

Not deductible: Fines or penalties charged by a lender. Those aren’t interest.

Not deductible: The cost embedded in a merchant cash advance structured with a factor rate instead of interest. There’s no interest to deduct.

Documentation‑Based Eligibility Tests for Deducting Working Capital Loan Interest

To claim the deduction, the IRS requires proof that your loan is real debt, not a gift or an equity investment dressed up as borrowing. You need a bona fide debtor–creditor relationship. That means formal paperwork, market‑rate interest, and a clear repayment schedule. If the loan looks like a handshake deal with no enforceable terms, the IRS can disallow the deduction.

Documentation is how you prove it. Keep the promissory note, the loan agreement, and any amortization schedule the lender provided. You’ll also need lender statements showing interest charged and payments made, plus your own bank records proving the funds were spent on business items. If you ever face an audit, these records are what stand between you and a disallowed deduction.

The IRS wants to see that repayment is happening and that the terms are reasonable. If the interest rate is wildly above or below market norms, or if there’s no fixed repayment plan, the loan may not qualify.

IRS Criteria for Bona Fide Debt:

Legal liability: You must be legally obligated to repay the debt. The lender has enforceable recourse if you default.

Formal loan documents: A signed promissory note or loan agreement with clear terms. Principal amount, interest rate, payment schedule.

Reasonable interest rate: The rate should be consistent with market rates for similar loans. Too high or too low can signal a sham transaction.

Intent and evidence of repayment: Regular payments deposited by the lender, cancelled checks or ACH records, and ongoing compliance with the repayment schedule.

Timing Rules and How Interest Becomes Deductible for Working Capital Borrowing

The timing of your deduction depends on your accounting method. Cash‑basis taxpayers deduct interest in the year they actually pay it. Accrual‑basis taxpayers recognize interest expense when the obligation becomes fixed and determinable, even if payment happens later. Most small businesses use cash basis, so the rule is straightforward. You deduct the interest when you write the check or make the ACH transfer.

One common confusion is the difference between principal and interest. When you make a loan payment, part of it goes toward paying down the loan balance (principal) and part covers the cost of borrowing (interest). Only the interest portion is deductible. For example, if your monthly payment is $2,000 and $1,500 of that is principal while $500 is interest, you can deduct the $500. The $1,500 doesn’t reduce your taxable income.

Year‑end accruals can come into play if you’re on accrual accounting and interest has been incurred but not yet paid. As long as the liability is fixed and the amount is determinable, you can recognize that interest expense in the current year even if you pay it in January. Cash‑basis businesses don’t get that option. They wait until they pay.

| Description | Treatment |

|---|---|

| Principal portion of loan payment | Not deductible; reduces loan balance only |

| Interest portion of loan payment (cash basis) | Deductible in year paid |

| Interest incurred but unpaid (accrual basis) | Deductible when liability fixed and determinable |

Documentation and Recordkeeping Required for Short‑Term Working Capital Loan Interest

The IRS expects you to prove that your loan is legitimate and that the interest you’re deducting is tied to actual business spending. That means maintaining a paper trail from the moment you sign the loan agreement through the final payment. If you can’t trace borrowed funds to business expenses, the deduction is at risk.

Start with the loan agreement and any promissory note. Keep copies of the lender’s amortization schedule or any year‑end interest statements they send. You’ll also need bank statements showing loan proceeds hitting your account and then being spent on business items. Invoices, payroll records, rent receipts, whatever documents prove the money went to operations. If you have a UCC‑1 filing (common when the loan is secured by assets), keep a copy of that too. For mixed‑use loans where some portion went to personal expenses, prepare an allocation worksheet showing how you calculated the business percentage.

Required Documents Checklist:

Signed loan agreement or promissory note with interest rate, term, and repayment schedule.

Lender account statements showing interest charged and payments made.

Bank statements and cancelled checks or ACH records proving payments to the lender.

Invoices, receipts, payroll journals, or other records proving borrowed funds were spent on business expenses.

Amortization schedule or lender year‑end interest summary.

Allocation worksheets for any mixed‑use loans showing business vs. personal use percentages and methodology.

Deductibility Rules by Loan Type for Short‑Term Working Capital Financing

Different loan structures create different deduction patterns. Understanding which type you have helps you report correctly and avoid surprises at tax time.

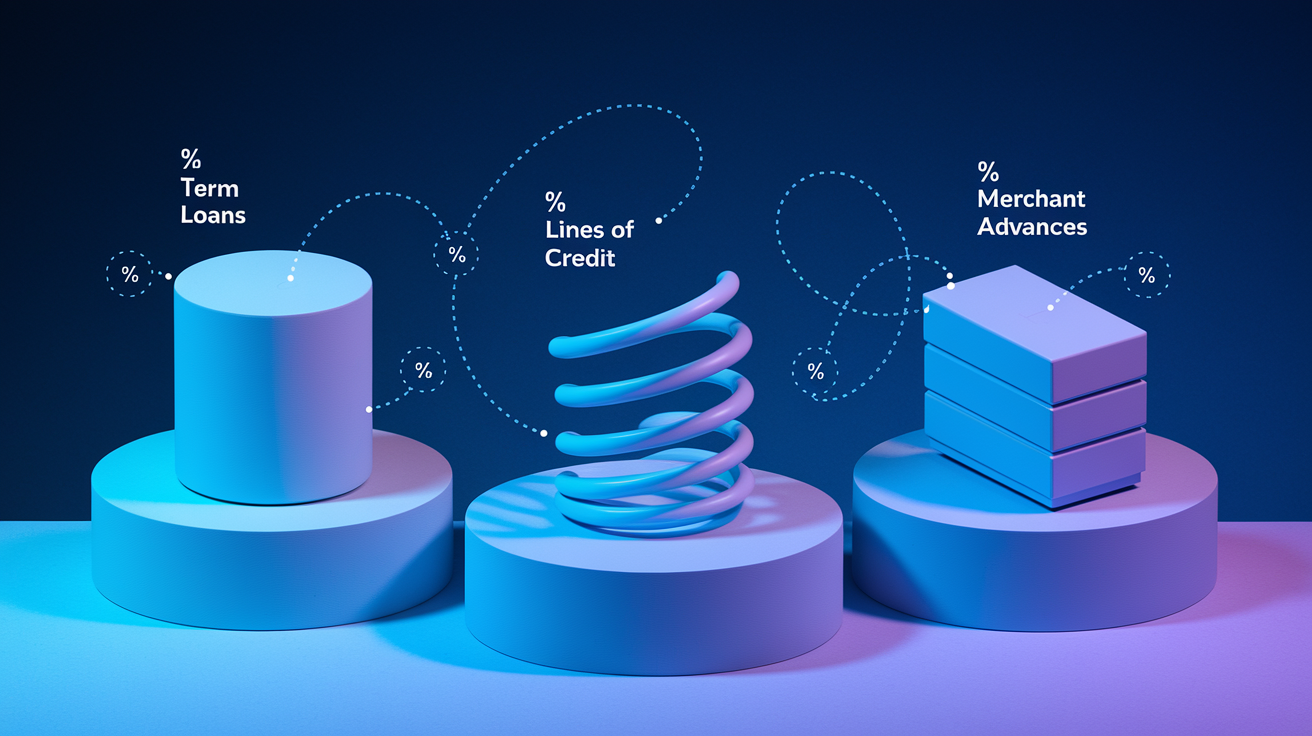

Term Loans

A term loan is a lump‑sum loan you pay back over a fixed period, often 3 to 10 years, sometimes longer. Each monthly payment includes principal and interest, with interest typically higher at the start. You deduct the interest portion in each tax year according to your amortization schedule. If you took out a 3‑year term loan in January, you’ll deduct the interest paid during that calendar year on your return.

Short‑Term Working Capital Loans

Short‑term loans usually have repayment periods of about 3 to 12 months. Because the full loan is repaid within a single tax year or slightly longer, you can typically deduct all the interest paid in the year you paid it. These loans are common for seasonal businesses or one‑time expenses like a large inventory buy. The IRS treats them the same as any other business loan. Interest is deductible when paid, as long as the funds were used for business.

Lines of Credit

A line of credit gives you a borrowing limit, but you only pay interest on what you actually draw. If you have a $30,000 credit line and you draw $5,000, you’ll pay interest on the $5,000. You can deduct the interest on the amount you used during the tax year. If you draw funds in December but don’t spend them until January, the deduction follows the spend date, not the draw date.

Personal Loans Used for Business

You can deduct interest on a personal loan if you used the proceeds for business purposes. The key is allocation. If 60% of the loan funded business expenses and 40% went to personal use, you can deduct 60% of the interest. You’ll need detailed records showing how the funds were split and supporting documents for the business expenses.

Merchant Cash Advances & Factoring

Merchant cash advances are advances on future sales, typically priced with a factor rate rather than an interest rate. Because the repayment structure is tied to a percentage of daily credit card sales or receivables, there’s often no stated interest to deduct. Invoice factoring works similarly. The factor buys your receivables at a discount, and the fee is usually not treated as interest. Invoice financing, where you borrow against receivables with a traditional interest charge, does create deductible interest.

| Loan Type | Deductible? | Notes |

|---|---|---|

| Term loan (business use) | Yes | Deduct annual interest per amortization schedule |

| Line of credit (drawn and spent) | Yes | Only on amounts actually used for business |

| Personal loan (60% business use) | Partial | Deduct 60% of interest with allocation records |

| Merchant cash advance (factor rate) | Generally no | No traditional interest to deduct |

Limitations on Interest Deductions: Section 163(j), TCJA, and Large‑Business Thresholds

The Tax Cuts and Jobs Act introduced Section 163(j), which limits business interest deductions for larger companies. If your business exceeds a certain gross receipts threshold (currently $32,000,000 for 2026, adjusted annually), your net business interest deduction may be capped at 30% of your adjusted taxable income for the year. That means even if you paid $100,000 in interest, you might only be able to deduct a portion of it this year, with the rest carried forward.

Small businesses are generally exempt. If your average annual gross receipts for the prior three years are below the inflation‑adjusted threshold (historically $25 million baseline, now higher), Section 163(j) doesn’t apply to you. Most working capital borrowers fall under this exemption. But if you’re growing fast or you operate multiple entities, check the three‑year average.

There are also thin‑capitalization and related‑party loan rules. If your business is heavily leveraged with debt from owners or affiliates, or if your debt‑to‑equity ratio is unusually high, the IRS may scrutinize the structure. In extreme cases, loans can be recharacterized as equity. That means interest payments become nondeductible dividends.

When Section 163(j) Applies:

Your business’s average annual gross receipts over the prior three tax years exceed the inflation‑adjusted threshold (e.g., $32 million for 2026).

The limitation caps net business interest expense at 30% of adjusted taxable income (ATI).

Disallowed interest can be carried forward indefinitely to future tax years.

Real estate businesses and certain regulated utilities may elect out of the limitation under specific conditions, but with trade‑offs in depreciation treatment.

Reporting Interest Deductions by Entity Type (Schedule C, Form 1120, Form 1065)

How you report your interest deduction depends on your business structure. Sole proprietors and single‑member LLCs report business interest on Schedule C, Form 1040. You’ll enter the total interest paid for the year on the appropriate line, and it reduces your net profit subject to self‑employment tax and income tax.

Partnerships and multi‑member LLCs taxed as partnerships file Form 1065 and report interest expense on the partnership return. Each partner receives a Schedule K‑1 showing their allocated share of the interest deduction, which they then report on their personal returns. S corporations follow a similar pattern. Form 1120‑S at the entity level, with K‑1 allocations to shareholders.

C corporations report interest deductions directly on Form 1120. The deduction reduces corporate taxable income at the entity level. C corporations also have slightly different rules for some types of interest, including certain interest on loans used to pay corporate taxes, which can be deductible in limited circumstances.

Entity Reporting Summary:

Sole proprietors / single‑member LLCs: Schedule C (Form 1040), line for interest paid.

Partnerships / multi‑member LLCs: Form 1065; interest allocated to partners via Schedule K‑1.

S corporations: Form 1120‑S; interest allocated to shareholders via Schedule K‑1.

C corporations: Form 1120; interest deducted at the corporate level.

Examples of Deductible vs. Non‑Deductible Interest for Working Capital Loans

Seeing real scenarios helps clarify where the line falls. A restaurant that borrows $50,000 to cover payroll and food costs during a slow winter can deduct all the interest paid that year, assuming the loan was spent on those business expenses. A contractor who takes out a personal loan and uses 85% of the proceeds to buy tools and materials can deduct 85% of the interest, as long as they have records proving the business allocation.

On the flip side, if you borrow money and leave it sitting in a savings account, the IRS won’t let you deduct the interest. Even if you plan to spend it on business later. The spend has to happen first. If you refinance an old loan and use the new loan proceeds to pay off the interest owed on the old loan, you can’t deduct that interest payment. The new loan’s interest is deductible going forward, but not the interest you paid with borrowed money.

Penalties and fees that aren’t interest also don’t qualify. If your lender charges a late fee or an origination penalty, those aren’t deductible as interest. And merchant cash advances structured with a factor rate instead of an interest rate typically don’t create any deductible interest at all. The cost is baked into the repayment amount, but it’s not classified as interest for tax purposes.

| Scenario | Deductible? | Reason |

|---|---|---|

| $50,000 working capital loan used for payroll and inventory | Yes | Funds spent on legitimate business expenses |

| Personal loan where 60% of proceeds used for business equipment | Partial (60%) | Must allocate interest by business‑use percentage |

| Loan proceeds sitting idle in bank account | No | Treated as investment; interest not deductible until funds spent |

| Refinance loan used to pay interest on prior loan | No | Cannot deduct interest paid with borrowed money |

| Merchant cash advance with factor rate (no stated interest) | No | Factor rate is not classified as interest |

Compliance Risks, Audit Triggers, and Best Practices for Interest Deductions

The IRS looks closely at interest deductions when documentation is weak or when the loan structure doesn’t look like arm’s‑length debt. Common red flags? Loans with no repayment schedule, interest rates that are far outside market norms, related‑party loans where the borrower and lender are family members or commonly owned entities, and situations where borrowed funds can’t be traced to business use.

Refinancing errors are another risk. If you use a new loan to pay off the interest on an old loan, and you deduct that interest payment, the IRS can disallow it. You also can’t deduct interest on loans used to pay personal income taxes or penalties, except in limited cases for C corporations. If you have a mixed‑use loan and you don’t maintain clear allocation records, the IRS may disallow the entire deduction rather than allow a partial one.

The best way to stay compliant is to keep detailed, contemporaneous records. Document the loan at the time you take it out, track the spend as it happens, and reconcile your lender statements with your books each year. If you ever restructure a loan or refinance, note the new terms and make sure your accounting reflects the change correctly.

Best Practices to Avoid Audit Issues:

Maintain complete loan documentation from origination through final payment, including promissory notes, amortization schedules, and lender statements.

Trace every dollar of borrowed funds to specific business expenses using invoices, receipts, and bank statements.

Use separate bank accounts for business and personal funds to avoid commingling that complicates allocation.

For related‑party loans, document arm’s‑length terms and ensure the interest rate and repayment schedule are commercially reasonable.

Reconcile lender interest statements with your books quarterly, and prepare allocation worksheets for any mixed‑use loans before you file your return.

When to Consult a Tax Advisor Regarding Working Capital Loan Interest

Some situations are straightforward. Others have enough complexity that a CPA or tax attorney can save you money and headaches. If you’re anywhere near the Section 163(j) gross receipts threshold, you need professional help to calculate your three‑year average and determine whether the limitation applies. The ATI calculation and any carryforward of disallowed interest require detailed schedules that most business owners don’t prepare on their own.

Mixed‑use loans, especially personal loans used partly for business, require careful allocation and documentation. If you get the math wrong or can’t support your allocation, you risk losing the deduction entirely. Related‑party loans (borrowing from a spouse, parent, or another entity you control) require arm’s‑length documentation and market‑rate interest. The IRS scrutinizes these closely, and a tax advisor can help you structure and document them correctly from the start.

Scenarios That Warrant Professional Advice:

Your business gross receipts are approaching or exceeding the Section 163(j) threshold, and you need ATI calculations and carryforward tracking.

You’ve taken out a personal loan or home equity line of credit and used a portion for business. Allocation and tracing are critical.

You’re refinancing existing debt or restructuring loans, and you want to ensure the new interest remains deductible and prior interest isn’t double‑counted.

You have related‑party loans or debt from owners, and you need to establish arm’s‑length terms and protect the deduction from IRS challenge.

Final Words

When you close the loan and spend the money on payroll, inventory, or rent, the interest generally becomes deductible, provided you have formal loan documents, prove the funds were used for business, and follow timing rules.

This post walked through the core rules, the documentation tests, timing for cash vs accrual taxpayers, loan‑type differences, and the main limits to watch. Keep promissory notes, bank pulls, canceled checks, and invoices so you can trace every dollar.

For questions about the tax deductibility of interest on short term working capital loans, save your records and talk to a tax pro. With the right paperwork and timing, you’ll likely keep that deduction and protect cash flow.

FAQ

Q: Is working capital a short-term loan?

A: Working capital is the money you use for daily operations, not a loan. Lenders often provide short-term loans (typically 3–12 months) to cover working capital gaps when cash is tight.

Q: What are the biggest tax mistakes business owners make?

A: The biggest tax mistakes business owners make are mixing personal and business expenses, poor recordkeeping, misclassifying deductions, ignoring timing rules, and missing limits like Section 163(j).

Q: What types of loan interest are tax deductible?

A: Interest on loans used for legitimate business purposes is generally deductible if you’re legally liable and the funds are spent for business. Examples: loans for inventory, payroll, or rent; interest, not principal, is deductible.

Q: Do working capital loans have interest?

A: Working capital loans usually have interest or fees. Banks charge interest; invoice financing generally charges interest; merchant cash advances use factor rates (a flat fee). Deductibility depends on business use and documentation.